Cast Vs. AM: High Mix/Low Volume—And High Drama

Featured in AdvancedManufacturing.org and ME&T Manufacturing Magazine

Recently, I’ve leaned into the quote attributed to President Dwight D. Eisenhower that “plans are worthless, but planning is everything.” It strikes me as particularly relevant to the discussion of cast versus additive manufacturing (AM). It isn’t a discussion so much as hand wringing, coupled with both sides arguing mostly out of emotions rather than readily available data. Planning requires getting data. So, hold on, let’s take a data-driven, drama-free, do-si-do on castings and AM.

Castings aren’t dying; they are evolving. We have the best future when we accept the limitations of both and plan accordingly. Absent a plan to use both, little will change. We need to adapt, overcome and persevere.

Over the last two decades, North American foundries have navigated consolidation, customer offshoring and raw material volatility, while tonnage has stayed consistent with revenue generally trending upward. Many plants have closed, but the survivors tend to be larger, more automated and more productive, supporting a healthy base of profitable businesses rather than a distressed industry on life support.

In parallel, metal AM has grown from a niche prototyping method into a credible production option, with cost structures that remain high on a dollars-per-kilogram basis, but are improving. The tension between these two worlds is real, but do we know what problem needs a solution?

What Problem Are We Actually Solving?

Historically, casting buyers have two fundamentally different demand profiles: low-mix, high-volume (LMHV) programs that run for years, and high-mix, low-volume (HMLV) portfolios catering to spare parts and lower production. Foundries perform well financially for LMHV because they can amortize tooling, engineer robust processes and drive down unit costs through repeatability. But they struggle when every order is a one‑off.

At the same time, North American manufacturing faces a persistent workforce challenge, with skilled melt, molding and finishing expertise aging out faster than it’s replaced. The real problem is not “castings versus AM,” but “How do we keep supplying structurally sound, economically viable metal parts across LMHV and HMLV in a tight labor market?”

A 20‑Year Snapshot of Foundries

Industry studies show that U.S. and North American casting output has fluctuated with recessions and reshoring cycles but remains on the order of 10–11 million metric tons annually, putting the region among the top three global producers. Over about 20 years, the number of plants has dropped, while tons per plant and automation levels have increased, especially in high‑volume iron and aluminum operations.

Profitability, while cyclical, has benefited from this consolidation and productivity gain: Fewer, yet stronger, players now command modern plants, diversified customer bases and better pricing power. The tradeoff is reduced surge capacity and less appetite for small, messy programs that distract from core LMHV business (think defense).

AM, Dollars/Kg and the Multilaser Dilemma

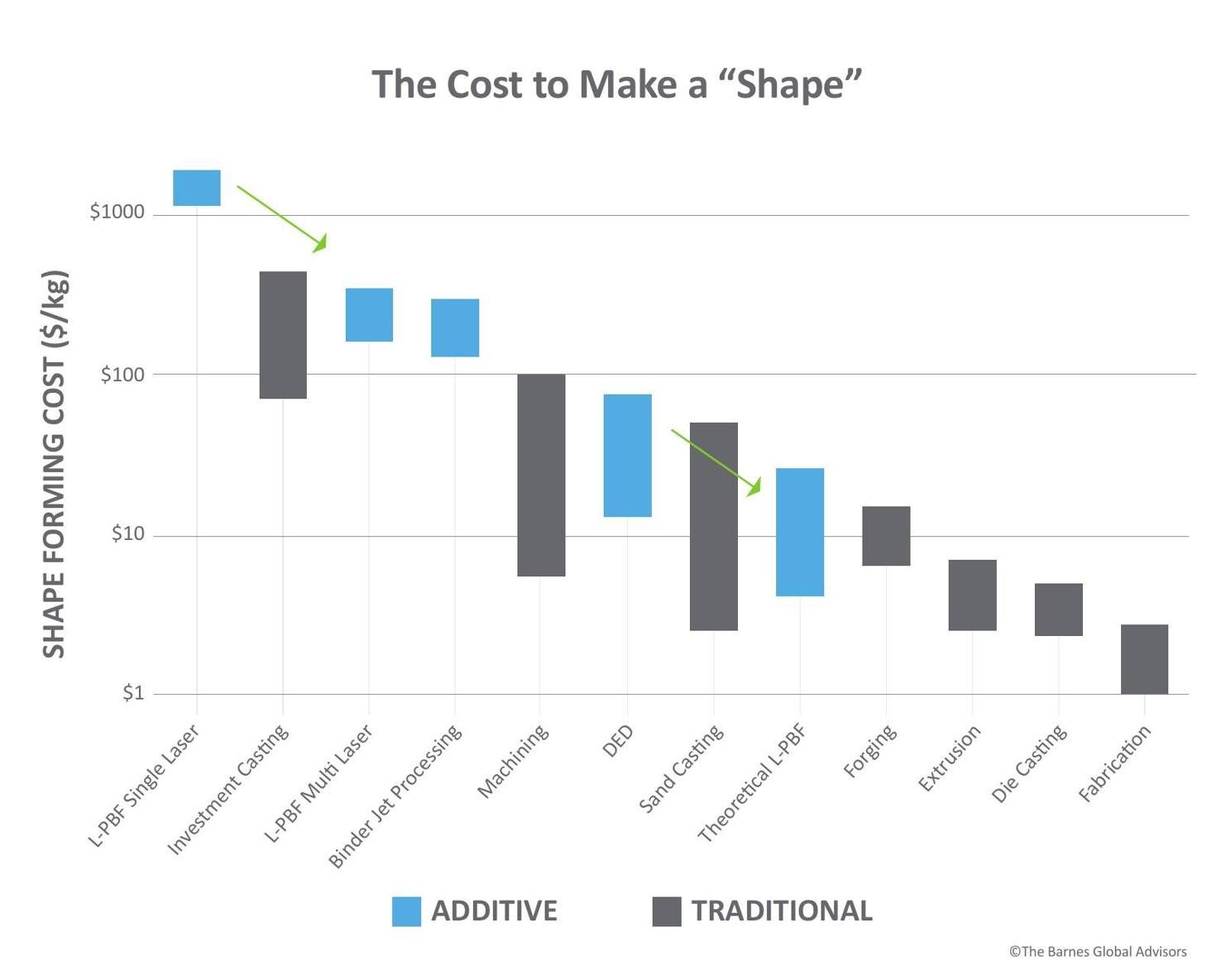

Metal AM economics still start from an uncomfortable position for production engineers. In‑house part cost estimates commonly sit in the $100-plus to $1,000 per kilogram for metal PBF (Figure 1), even before post-processing and qualification. Those numbers can be justified for highly optimized aerospace brackets or patient-specific implants. Still, they are unhelpful when trying to replace a casting sold at $10 to $100 a kilogram.

To close the gap, the industry has leaned hard into multilaser systems and larger build volumes, which promise more kilograms per hour and better machine utilization. The catch is that every added laser multiplies the qualification burden: testing, process maps, cross‑laser stitching and material property consistency all need to be proven and documented, part family by part family, for industries that are notoriously conservative. In other words, multilaser is necessary to drive down nominal cost per kilogram, but it raises the bar on process control, statistical evidence and ultimately trust.

Process Optimization

The way out is to stop asking AM to be cheaper at casting and start using each process where it is structurally advantageous. Foundries should own LMHV production—engine blocks, housings, brackets and structural parts where tooling is justified, geometries are known and millions of kilograms per year flow through optimized lines.

AM can then act as the scalpel for HMLV and workforce‑constrained niches:

Complex internal features that are impossible or risky in sand or investment molds

Spare parts where original tooling is gone or marginal

Bridge production while new casting tools are built or transferred

Capacity relief when foundries are short of skilled labor but long on engineering talent that can run digital workflows

If we pair that with serious work on multilaser qualification and general improvements to accelerate qualification with AM, we can achieve predictable costs and a reliable, repeatable process. Foundries, in turn, can integrate AM either in-house or through partners to offload problematic HMLV work, stabilize their labor model, and focus capital on areas that generate the best returns and output.

For 20 years, the story around castings and AM has been told in the language of threat: offshoring, plant closures, disruptive technologies waiting in the wings. And yet here we are: foundry tonnage comparable with two decades ago, a more profitable and consolidated base, and a metal AM sector that has proven it can deliver certified, high‑performance hardware.

It is time to move from anxiety to action.

Treat AM as the precision instrument for HMLV and workforce bottlenecks; not as a blunt replacement for castings.

Design in and double-down on casting’s LMHV strengths, and use AM to de‑risk spares, sustainment and complex geometries that strain foundry labor models.

Prioritize multilaser qualification and accelerated qualification methods to improve the economics.

Planning to achieve those actions would be indispensable. Imagine the conversation in another 20 years? It would be about adaptation, overcoming and perseverance—not survival. It will be about how people made a difference to keep critical manufacturing capacity, skills, and innovation anchored here at home and with our allies.